Indian Economy: Covid Second Wave & After

It is useful to compare India's second wave with the first wave, in analyzing its effect on the Indian economy. However, this analysis is incomplete, unless there is a better understanding of the speed and severity of the 2nd wave relative to the first (see previous blogs). It also requires an understanding of Pandemic and lock-down economics (see research & policy papers at foundation for economic growth and welfare (EGROW) website).

This note contains a preliminary analysis based on available data. Among the elements of this analysis is the comparison of Lockdowns/restrictions, the differential impact of pandemic on the three aggregates, essential goods, manufacturing, mining & construction & contact services, the unemployment comparisons, Income and wealth effects and their effect on private consumption, effect of skilled labor shortage and supply chain disruptions on inflation. The note concludes with implications for monetary and fiscal policy.

-

2020 Lockdown started on 20th March and shut down 60% of Indian economy, in 2021, lockdowns were narrower, State/District specific, starting in April. The lockdown arithmetic therefor suggests smaller effect of lock down on economy.

-

Essential goods were exempted from both lockdowns, so there is little reason to expect agriculture to be affected very differently, except for two exogenous. One global and Indian agricultural prices are much higher than a year ago, so this will have a positive effect on agriculture sector despite some increase in input prices as terms of trade are clearly better. The second is the rise real wages following, years of falling or stationary real wages. Both are a positive for rural economy in FY22. I think too much weight is being given to Covid wave effect on rural economy relative to urban economy. The fact that second wave has 4 times the cases of first wave, means that direct effects on health will be 4x what they were last time. Overall, the latter effect is short term while the former two are medium term, so agriculture will do better that in 1st wave, after an initial hiccup.

-

Conventional wisdom is that the Covid 2nd wave will follow the same pattern as the first wave. Our analysis shows that the second wave was faster and much more virulent in terms of numbers of cases and deaths and will therefore subside much more sharply and quickly than the first wave. There will therefore be an upside surprise to the economy.

-

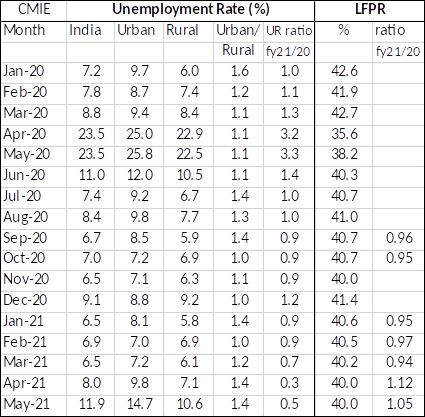

In first wave, unemployment rose to 8.8% in March, 23.5% in April & May and improving to 11.6% June as lockdown was eased (table 1). In 2nd wave, Unemployment rate rose from 6.5% in March to 8% in April and further to 11.8%. This is half of first wave peak, so direct effect of lockdown on production is about half of first wave! The ratio of the urban to rural unemployment rate in the second wave is 1.4 compared to 1.1 in the first wave. Urban areas have been hit harder than rural areas contrary to the assumption of most analysts. This is to be expected from our research on the State wise spread of the mutated virus causing the second wave, which showed that states with higher urbanization have been worse affected than less urbanized states.

-

Income effect: Post lockdown the Manufacturing-Mining-Construction sectors recovered rapidly after supply chains disruptions were addressed, as our research had predicted. Given the geographically and sector-ally more limited nature of the current restrictions/lockdown, supply chain disruptions are more limited in India, and there is recent experience of dealing with them, the recovery will be as, if not more, rapid. Supply chain disruptions are more widespread across the world and the consequent rise in oil prices will have a negative effect on national income & growth, but as usual this will be partly offset by higher exports and remittances.

-

Contact services (hospitality, entertainment, tourism) would take much longer to recover, because of the reality and the fears of infection, particularly in indoor venues and badly ventilated locations. Govts need to incentivize improved ventilation in outdoor venues as well as indoor public spaces & factories & offices, installation of high-quality air filters in air-conditioned halls & buildings and Ultra-Violet (UV) ceiling lights in crowded, small rooms (pubs, bathrooms, kitchens, restraints).

-

Wealth effect(negative): Saving, Consumption: The first wave eliminated the meagre accumulated savings of the poor. The second wave has done the same for many lower middle-income households as well as the middle-income families affected by disease and death. The precautionary savings are therefore expected by many analysts to increase, post second wave, and thus delay the recovery of private consumption. There are however three other factors one negative and two positive that need to be considered to derive the net effect on consumption.

-

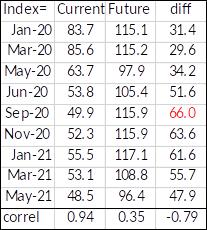

Consumer Expectations: The consumer confidence incidence (RBI survey) fell from 86 in March 2020 to a low of 50 in September 2020 and had recovered to 55.5 by Jan 2021 & declined to 53.1 in March 2021 (table 2). This will be a negative factor in the speed of recovery of private consumption after lockdown. Interestingly, the gap between the current and future expectations index has more than doubled since pre-covid days and may result in a fast reversion in current expectations, once it starts. Institutions providing consumer credit (e.g. NBFCs) are in a much healthier position than they were 18 months ago, while credit demand from corporations for bank credit is low, given higher internal savings. So, consumer credit will aid recovery. There was no vaccination in sight through much of the first wave. There are now several approved vaccines, including two produced in India, with several more on the way. The planning & management problems which have slowed vaccination are manageable and will be solved. So, the medium-term income growth trend is much more positive than during the first wave. Both these factors will offset the desire for more precautionary savings.

-

Skilled labor effect: In the second wave, Severe Covid cases and deaths are four times that in the first, and the urban middle class has been more heavily impacted. It is therefore possible that pre-existing shortages of skilled labor will be accentuated, negatively affecting the speed of recovery of industry & services for which demand recovery is quick. Govt should quickly implement the changes in the Apprentice ship act announced in budget, and to improve training of semi-skilled workers in cooperation with industry.

-

Across the World (including India) supply chain disruptions and short-term adjustments in demand (e.g. diversion of demand from contact services to goods, because of contagion fears) have led to inflationary pressures in particular goods or sets of goods. These pressures are temporary and will subside as Covid contagion fears decline and demand patterns normalize in 2021. The long-term increase in Govt infrastructure investment in USA is a different aspect, whose effect on inflation needs to be assessed separately.

-

Overall, GDP growth in Q1 of FY22 will be lower than projected in March 2021, and investment revival delayed by one quarter. As consumption depends on expected income, which is clearly on an upward trajectory in H1 of FY22 as against the downward trajectory in H1 of FY21, this factor will offset the impulse to increased precautionary savings, from Q2 of FY22. Recovery will be much faster in Q2 than anticipated by forecasters. FY 2022 GDP growth will remain within the range of 10% +/- 1.5%, even though the downside risk appears much higher at this point, than it was in February 2021.

-

Fiscal deficits are being driven by GDP linked revenue fluctuations, which act as automatic stabilizers. The best fiscal stimulus that Govt can provide is revenue neutral or revenue negative tax reform, by accelerating simplification of GST towards a single rate (15%) for 75% of G&S, introducing a new direct code. Speedy revival of construction intensive infrastructure projects will help normalization of total employment. Incentives for air filters & UV lights and investment/production/distribution of Covid vaccines, will help reduce the chances of a third wave, reduce fears of contagion and restore consumer confidence. Govt can speed the recovery, by implementing the apprenticeship act reform announced in budget and completing Ease of compliance of Labor, tax & financial laws & rules, which it has previously promised. Central govt should also review the laws, rules and regulations affecting start-ups and tech companies to make them competitive with other locations like Singapore. State governments must do their part in simplifying the jungle of controls and regulations imposed by them, and speeding up the vaccination process.

-

Monetary policy is and has been on the right trajectory since the start of the pandemic and should continue the same path. Only fine tuning of credit policy or govt security markets may be needed.

Table 1: Unemployment and LFPR

Table 2: Consumer Confidence Survey (RBI)