Webinar held on Pre-Budget Discussion

Key suggestions

- MSMEs are strategic and finance is a challenge

- Boosting infrastructure and using Block Chain Technology extensively

- Focus on Quality of Public Expenditure

- Fiscal Consolidation needs to be pursued

- Supply side management is important for agriculture

- Anganwadi system needs to be strengthened

- North East needs a special package

- Optimal mix between Fragile Mountains versus Development

- Examine why funds are under utilized?

- Establish Debt Market Exchange to boost Corporate Bond Market

- Environment & Pollution in small cities also need attention

Detailed Views by the Panellists

1. M.P. Bezbaruah, Associated Faculty, Economics, Gauhati University

- The economy continues to sustain high growth alongside low inflation, which is a strong positive indicator of the macroeconomic situation

- Although the exchange value of the rupee has been declining, this is not necessarily alarming. Such movements have been taking place continually since the INR has been made a floating currency in early 1990s. At the present context of rise of protectionism all around, this may be a blessing in disguise as this protects our exports to some extent.

- The government is expected to continue its strategy of maintaining high capital expenditure, which is essential for two reasons. First, despite progress, India’s infrastructure development still has significant gaps . Second, capital expenditure has a strong income-generating multiplier effect on the economy.

- Another important area that needs attention is the quality of public expenditure. Improving spending efficiency—particularly in education and health—is crucial. Targeted reforms and initiatives in these sectors would yield long-term benefits.

- A growing concern in the economy is the rise of monopolies or oligopolies, evident in sectors such as telecom and aviation, where effective competition is often limited to just two major firms. Such concentration can undermine efficiency and innovation in the long run. Policymakers must focus on preserving competitive markets rather than allowing excessive consolidation.

- Rising inequality remains a serious concern. The government’s provision of free food grains has offered much-needed relief and ensured basic consumption security. However, such measures cannot be a long-term solution to inequality. A more fundamental approach is required to integrate more people into stable, formal employment.

- Both central and state governments are increasingly relying on income transfers. While this approach has gained attention globally—especially in light of technological change, AI, and potential job displacement—the current system in India is fragmented and ad hoc. If income transfers are to become a permanent feature of the economy, they should be designed within a systematic framework, such as a Universal Basic Income (UBI) model, rather than through scattered schemes.\

2. C.L. Dadhich, Former Director of Research, Reserve Bank of India

Importance of Rural Sector

- Rural Sector is one of the important sector of the Indian Economy.

- It’s share in the Budget is not commensurate to it’s importance

- It deserves some special treatment

{kind=link}

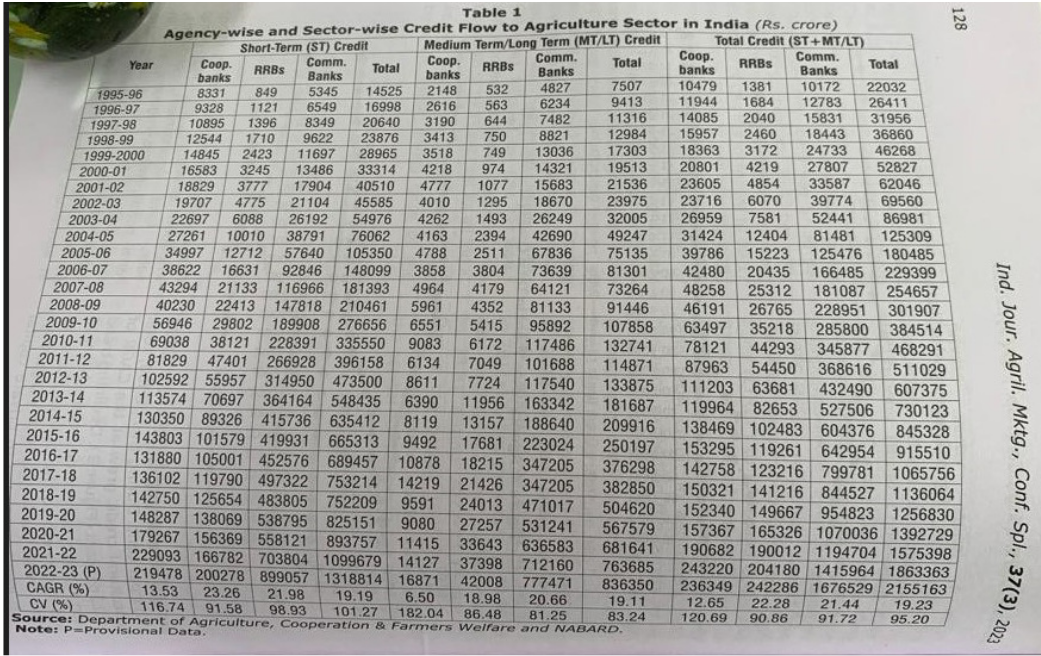

Credit Flow to Agriculture

- Agency wise credit flow to agriculture from 95-96 to 20-23 as given in table 1. Indicates, that in 1995-96 co-operative banks purveyed highest amount of Rs 10,479 crore, closely followed by commercial banks. The share of RRB was much lower at Rs 139 crore

- In 95-96 short term credit was highest in case of co-operative banks at Rs 8,331 crore distantly followed by commercial banks at Rs 5,348 crore and RRBs only Rs 849 crore.

- Volume of investment credit (MT/LT) was highest for the commercial banks at Rs 4827crore distantly followed by co-operative banks, RRB share was much lower at Rs 532 crore

- Scenario of credit flow to agriculture witnessed a sea change over the years with overall growth rate of 19% (RRBs 22%, Commercial banks 21% and co-operative banks 13%)

- Short term and investment credit flow grew almost at par.

- In 22-23 agency wise commercial banks accounted for highest credit of Rs 16.8 lakh crore distantly followed by RRB’s Rs 2.42 lakh crore and Co-operative banks at Rs 2.36 lakh crore.

In short, following observations can be made

- Over the years flow if short term expanded in terms of the volume while investment credit could not keep pace with short term credit. This is not a healthy sign. Perhaps interest subvention on short term credit has contributed to this phenomenon

- Commercial banks emerged as a main player for both short term and investment credit leaving co-operative banks and RRBs much behind.

Major Policy Innovations in Rural Credit

- Interest Subvention

- Directed Credit

- Kisan Credit Card

Interest Subvention

- In order to encourage commercial banks to provide crop loans at 7% it was decided in 2006-07 to provide interest subvention of 3% (Since modified to 1.5%). However, later 3% interest subvention was given on prompt repayment as well. Apart from crop loans interest subvention was extended to working capital loans for animal husbandry and fisheries.

- The scheme has augmented flow of crop loans.

- However, in the absence of interest subvention on term loan its lending has been adversely affected.

- Intriguingly, micro-finance institution and micro-finance borrowers are not covered under the scheme.

Directed Credit

- After nationalization of 14 major commercial banks SCB were directed to provide atleast 33% of net credit to priority sectors like agriculture, cottage industries, small transporters etc. Later target was raised to 40% with sub-targets for agriculture direct and indirect finance for agriculture, tiny and cottage industries etc. Public sector banks performed better than private sector banks

- However, targets were not strictly enforced as it is being followed in case of Cash Reserve Ratio and Statutory Reserve Ratio.

- Later on SCBs were required to deposit short falls in their agricultural lending with NABARD in a fund known as RIDF to finance rural development projects at an interest rate lower than priority sector lending rates.

- As repayments were fully guaranteed, banks prefer to invest in RIDF. Banks also save on cost as financing large accounts involves lower cost. This has adversely impacted the flow of credit at grass root level as financing involves higher cost and risks

- As at end March 2023, balances in RIDF amounted to Rs 1,63,069 crore forming about one-fifth of resources of NABARD.

- It goes without saying rural infrastructural development projects should be financed through budgetary resources rather than curtailment of credit to farmers.

- In the wake of financial sector reforms with a view to reducing risk of priority sector lending its definition was enlarged to include less risky activities such as investment in select bonds, agro-industrial units etc

- Broadening definition of priority sector has dilutes the very concept of priority sectors at cost of needy and poor.

Kisan Credit Card

Kisan credit card scheme was introduced in 1998 to provide hassle free credit to farmers on the pattern of cash credit limit prevailing in case of business finance. This also has the advantage of interest on balance outstanding unlike crop loan system.

- Of-late with the launching of Rupee card, framers have all the advantage of payment through card for their purchases.

- On pattern of KCC similar card is also issued to non-farmers in rural areas known as General credit card

- As at end March 2025 there were as many as 7.7 crore operative KCC with outstanding of 10.0 lakh crore crop loan accounted 88% of total outstanding distantly followed by term loan 8% and working capital loans to animal husbandry and fisheries at 4%. The share of operative KCC was around 50% involving 2/3rd of amount outstanding.

- This suggests that one third of amount outstanding under KCC was NPAs.

- This in context, the possibility of on-lending by beneficiaries to other needy farmers to earn interest arbitrage (borrowing at 7% per annum and on-lending at 24% per annum) cannot be ruled out.

Major Findings of All India Debt and Investment Survey 2019

The share of institutional agencies has registered a rise from 56.8% in 2012 to 66.1% in 2018.(it was at peak of 69.4% in 1991) contrastingly the share of non-institutional agencies in rural indebtedness has witnessed fall from 44% to 33.9% during the period under review.

- Agency-wise commercial bank accounted for highest share 41.9% distantly followed by credit Co-ops (9.9%), MFIs (5.9%) and RRB’s (5.7%).

- Incidence of households indebted was higher at 40.3% in case of cultivator as compared to non-cultivator (28.2%). This suggests institutional agencies have a penchant for cultivator households.

- Dependance of non-cultivator was higher on non-institutional agencies as compared to institutional agencies

- Asset group wise institutional agencies have higher preference for higher asset brackets while non-institutional agencies were neutral across asset size.

- Social group wise incidence of indebtedness was higher among OBC class followed by upper class, SCs & STs.

Anganwadi Scheme

Scheme has made its presence felt in rural area but requires some improvements

- Reduction in the area of operation of Anganwadi

- Improve the promotion opportunities of staff

- Add new contents like success stories of great people

- Need for further increase in nutritional supplements

Senior Citizens

The percentage of Senior Citizens is gradually rising from 8% in 1951 to 11% in 2011

- Budgetary provision for Senior Citizens is about 1.5%

- Gainfully utilize the talent and services of Senior Citizens

- More and more day centers for Senior Citizens may be opened

3. Lt. Gen. R.S. Reen (Retd.), Former DG DGQA Officer, Ministry of Defence, GoI

1. R&D Spending

India is doing well in capacity building and we are not looking into innovation and new design.

The leading Indian corporates need to fund R&D innovation centres in different cities. These can be sector-specific and industry specific nassociations like FICCI and CII should drive this and Corporate to fund it .

The Government should drive it and give incentives for infrastructure development in respective State and stop migration of highly skilled technical man power

Have innovation and design centre in each states

IIT/ IIM to have start up incubator in each states . Giving priority to State base problem and finding innovative solutions .

2. Big Business Parks & Urban Concentration

Big business parks and software companies have come into three metro centres and three other cities namely Bangalore, Hyderabad and Pune. The growth is being driven and does not match with the urban city master plan.

These cities are choked due to the excess influx of the population, leading to pressure on environmental quality and higher pollution. Today, Delhi and the NCR region have unprecedented AQI levels and the city has expanded to 80 km in Radius .

Solutions to the Problem

- Make business parks at mega scale in all state capitals or cities chosen by respective states.

- Centre and State to make budgetary provision to arrest the population exodus of skilled youth by creating parallel development offices in each state which are digitally connected.

This will stop skewed growth in a few cities only.

3. Agriculture Sector

The agriculture sector is called the backbone of the country. Farmers need support in terms of technology for new-age farming.

a) Market-based research on what to grow

b) Identify the market for sale

c) Cold storage chain to avoid waste of seasonal crops

With a lesser shelf life, in states like J&k , Punjab movement of fruit by special goods trains to mandis across the country.

4. Free Trade Agreement

State who is grown in the agricultural commodities should not be impacted only regions which do not have that product o produce can import

Example: Cheaper import can import apples from NZ, can happen for Channai not for Delhi because it get enough from J&K / Himachal.

5. Retail Cost & Tax

There are different costs and taxes of a few products sold in different states. This leads to smuggling or selling in the black market.

Petroleum products and liquor have different rates in J&K & Punjab, Delhi & Haryana. So smuggling happens in inter-district borders. Uniformity of rates and tax in budget can control this problem.

4. Dilip Chenoy, Chairman, Bharat Web3 Association

From an industry perspective. It largely covers five different themes.

- Tax Certainty and Simplification

- Boosting investment and Manufacturing

- Addressing MSME issues

- AI, Web 3 and Frontier technology

- Tourism

1. Tax Policy and Administration Reforms:

• Dispute Resolution and Litigation Reduction:

• Implement statutory timelines for disposing of income tax appeals, specifically by the Commissioner of Income Tax (Appeals).

• Prioritize the resolution of high-value cases and permit virtual hearings.

• Introduce a One-Time Settlement (OTS) scheme for legacy customs-related disputes.

• Tax Deduction at Source (TDS) Rationalization:

• Simplify the TDS framework, proposing consolidation of rates into a few slabs (e.g., 0.1%, 2%, 10%) including for the VDA Sector.

-

Allow set off of losses for the VDA Sector.

• Exempt Business-to-Business (B2B) payments from TDS/TCS if they are already reported under the Goods and Services Tax (GST) framework to free up working capital and reduce compliance burden.

• Corporate and Manufacturing Tax:

• Extension of Concessional 15 % Corporate Tax Rate (similar to Section 115BAB) for new manufacturing units and potentially extend this benefit to Global Capability Centres (GCCs).

• Introduce a similar concessional tax regime for fresh investments and capacity expansion by existing firms.

• Indirect Taxes

• The announcement of Customs reform is a welcome step. A goal could be a "paper-free customs" environment by 2028

and better implementation of a single-window digital compliance portal to reduce border friction.

2. Boosting Investment, Manufacturing, and Infrastructure

-

Infrastructure and Capex:

• Propose a significant increase in Central capital expenditure (e.g., a 12% rise) and capex support to states.

• Announce the launch of a new National Infrastructure Pipeline (NIP) 2.0 for the next five to six years.

• A permanent dispute resolution mechanism for Public-Private Partnership (PPP) and infrastructure projects to unlock stalled assets.

-

Manufacturing

1. Create a ₹50,000 crore Sovereign Guarantee Window

For state/ULB green, mobility, housing, and industrial bonds—off-budget, low fiscal cost, high capex multiplier.

2. Mandate 5–7% Pension & Insurance Allocation to Infrastructure & Manufacturing Bonds with credit enhancement and risk-weight clarity to unlock ₹10–15 lakh crore of long-term capital.

3. Launch a National Manufacturing Financing Corporation (NMFC) To provide 15–20-year, low-cost debt for semiconductors, green steel, hydrogen, textiles, and Industry 4.0.

4. Restore Weighted R&D Deduction (200%) for Clean & Strategic Manufacturing; Focused on green steel, hydrogen, semiconductors, advanced materials, AI-led manufacturing.

5. Announce PLI 2.0 for High-Value Manufacturing Only

Target semiconductors, power electronics, specialty steels, technical textiles, energy storage—no volume subsidies.

6. Introduce Accelerated Depreciation for Green & Automated Capex

Covering energy-efficient machinery, robotics, recycling, CCUS, and digital manufacturing systems.

7. Announce a Green Steel & Industrial Decarbonisation Mission With viability-gap funding for hydrogen, scrap-based EAFs, CCUS pilots, and green public procurement norms.

3. Support for MSMEs and Credit Flow

Micro, Small, and Medium Enterprises (MSMEs) continue to demand measures to ease the flow of capital and simplify regulatory compliance.

-

Easier Access to Credit:

• Expand Credit Guarantee Schemes: Increase the scope and funding of credit guarantee schemes (like CGTMSE) to encourage banks and NBFCs to offer more unsecured loans.

• Promote cash-flow-based lending utilizing the digital public infrastructure (like Account Aggregators).

• Provide targeted credit enhancement for NBFCs lending to MSMEs to help reduce their borrowing costs.

• Tackling Delayed Payments (A major priority):

• A block chain based tokenised Bill system. Expand the pilot developed by IBDIC

• Technology and Compliance:

• Set up Mega Plug-and-Play Manufacturing Clusters (Budget-backed SPVs) With pre-cleared land, common utilities, testing labs, and multimodal logistics—time-to-production under 18 months.

-

Set up and Fund an MSME Technology Upgradation Mission (₹20,000 crore) Cluster-based rollout of automation, quality systems, compliance-as-a-service, and digital tools.

• Set up a single, unified compliance portal to manage all licenses, filings, and approvals.

4. Web 3 Sector

- Reduce TDS to 0.1%

- Allow set off of losses on VDA’s

- Enable easy registration and Banking rails to enterprises in the sector.

- Announce a regulatory framework or self-regulatory mechanism for the VDA Sector.

- Launch a National Regulatory Sandbox for AI, Web3 & Frontier Tech Single-window sandbox under MeitY/NITI with time-bound approvals for manufacturing, finance, and exports do not exclude crypto.

- Task each ministry to develop one Blockchain, AI + Blockchain application project that has potential to scale. For example, detecting counterfeit medicine Jan Ashudhi Kendras.

5. Tourism

- Launch a Heritage India Campaign for top 10 circuits;

- Allocate funds for quick fix upgrades for 20 Global facing sites.

- Encourage the development of State Tourism delivery units by means of a challenge fund.

- Launch a segmented global campaign using digital influencers.

- Develop a National Tourism Digital Platform.

One final point:

Typically, a budget allocation is announced and then once budget is approved the process for creating the scheme commences. This in many cases may take up to a year. Just yesterday, the details of a scheme announced in Budget 2025 were released. Perhaps a change could be introduced that whenever a budget recommendation is submitted, it must be accompanied by a draft scheme document which then could be finalised once budget is approved.

5. Ajit Pai, Strategy Lead Partner, Govt. & Public Sector, ST&T, EY India

All these reforms are more possible in this budget than future budgets, as they will be unpopular when announced and the economy will take 18-32 months to make the benefits highly visible and have material positive impact on the economy. With this budget, benefits will be visible well before the next general election, and the up front costs too far back to be relevant to electorate. It will get riskier in future budgets to take risks where the benefits take a couple of years to become evident in the economy and reap the benefits while costs will be fresher in people’s minds.

Broaden income tax base. Personal income taxes in India are still entirely contributed by less than 2% of the population even if about 8% of the population are filing returns, up from less than a third that a decade ago. Raising the tax paying threshold to Rs 12 lakhs (USD14k) is about the same as in the US.

Per capita GNI in India is a fifth that of the rate at which taxes begin. In the US, per capita GNI is about USD85k, over 5x the threshold for paying income taxes. Its time that India broadened the tax base, primarily to (i) reduce the general government debt to GDP that is currently about 80% relative to FRBM target of 60% (ii) improve visibility into the real state of the economy to better inform policy making and (iii) sustain high levels of investments in closing the infrastructure deficit in India. This can be done by (i) lowering the threshold for paying taxes to 3x the per capita GNI, (ii) Introducing taxation on agricultural income above Rs. 24 lakhs per year (2x the current threshold for non-agricultural income).

Reduce free food rations. A combination of MGNREGA and free food has created a material friction that is distorting the market for unskilled and semiskilled labor across the country as while by themselves each is a great facility/entitlement, together they are creating a threshold for workers to head to construction sites and other entry level manufacturing jobs. A reduction in beneficiaries and benefits to half the beneficiaries and half the benefits will boost labor markets in construction and manufacturing while reducing the number of workers in rural areas – massively boosting productivity in an economy with very low labour productivity.

Power reform. Power sector is still among the weakest links in India for enterprises to become more competitive. While the government has issues UDAY bonds to relieve pressure on state discoms, there is great reform required to boost infrastructure upgrades in capacity and reliability. GoI should start incentivising states to privatize the power sector and eliminate cross-subsidies by providing power free to agriculture and low consumption families and charging the lost revenue to industries, making them less competitive and not boosting employment. Any benefits to agriculture and low income families can be provided through direct benefit transfers that will be appreciate by the recipient even more while industries can be provided power at a rate commensurate with the cost of providing the service. Privatization can boost investment tremendously, to close the gap sooner, while improving efficiencies and competitiveness of enterprises in the state.

Disinvestment. GoI still has over 360 CPSEs many of which are not strategic to the GoI. Divestment of these have already been announced but it is going too slowly. Reaccelerating disinvestment will improve the fiscal position, bringing down the debt to GDP, it will reduce distortion in the economy by bringing the economy close to a market economy, and reenergize capital investment in the economy.

6. Prof. Kuldip Kaur, Economics, Guru Nanak Dev University

Two major challenges to agriculture that is supply, mismanagement and natural calamities need to be addressed in the forth coming budget.

Supply during the bumper crops can be checked by converting surplus produce into opportunity via production /diversification to crops,tailored to changing demand pattern of affluent class and by strengthening the entire value chain through making cold stores and processing the surplus.

The loss created by natural calamities like floods,droughts, etc.can be checked by creating climate, resilient infrastructure and systems.

Long term measures to leverage technology and nature are needed.

7. Prof. Indu Varshney, Economics, RMPS State University

In the context of global trade uncertainty, technological disruption, and supply-chain realignments, MSMEs require focused and forward-looking support in Union Budget 2026. MSMEs are not just small firms—they are central to employment generation, exports, and inclusive growth.

Let me highlight five priority areas where the Budget can make a decisive difference.

First, access to affordable finance.

This remains the most binding constraint. Budget 2026 should expand export credit and concessional financing, strengthen credit guarantee schemes, and introduce statutory collateral-free lending up to ₹1 crore for micro enterprises, with interest rates capped at 6–7 percent. This will directly address credit shortages and enable investment.

Second, technology adoption.

To remain competitive, MSMEs must adopt automation, digital tools, and cybersecurity solutions. The Budget should provide tax incentives or capital subsidies and launch a dedicated MSME Technology Upgradation Mission with awareness and hand-holding support.

Third, ease of compliance.

MSMEs face a disproportionate regulatory burden. A single unified digital compliance portal, decriminalisation of minor procedural lapses, and risk-based inspections would significantly improve ease of doing business.

Fourth, export promotion and risk mitigation.

MSME exporters are highly vulnerable to sudden tariff hikes and global shocks. An Export Risk Equalisation Fund would help micro exporters manage such risks, while enhanced export facilitation can improve access to global markets.

Fifth, logistics, infrastructure, and sustainability.

High logistics costs erode competitiveness. Investments in modern logistics, digital infrastructure, AI-based route optimisation, and inland waterways can reduce costs. Simultaneously, incentives for renewable energy and energy-efficient technologies will support sustainable MSME growth.

To conclude, Budget 2026 must treat MSMEs as strategic partners in India’s growth journey, not merely as recipients of support. A policy framework built on affordable finance, technology, regulatory simplicity, export resilience, and infrastructure will unlock MSME potential and strengthen India’s economic resilience.

8. Prof. Indraneel Bhowmik, Economics, Tripura University

1. Implementation challenges for NEP 2020: Infrastructure Deficit for several public funded HEls, special consideration for affiliating universities across the country: particularly needed for remote and rural universities... addressing digital divide

2. NER....

- a) plantation sector priortisation

- b) railway goods manufacturing- coaches, EMUs,

- c) aviation sector... use of airstrips as flying schools

- d) tourism- cultural, religious

- e) Sports and Music... soft power of NE.. harnessing

9. Rajeshwari U.R., Associate Professor, Economics, Christ University

Education and health are foundational pillars of human development and long-term economic growth. A pre-budget discussion that places these two sectors at the centre is essential, not only from a welfare perspective but also from the standpoint of productivity, demographic dividend, and inclusive growth. Despite improvements over the years, India’s performance on key education and health indicators continues to lag behind global benchmarks, highlighting the urgency for focused policy and fiscal interventions in the 2026 Budget.

Why Focus on Education and Health?

India’s health and education outcomes, when compared with global averages, reveal persistent gaps. Life expectancy in India stands at around 72 years, compared to a global average of 73.3 years. While this difference may appear modest, it reflects underlying disparities in access to quality healthcare, preventive services, and nutrition. Similarly, India’s literacy rate of about 82% falls well short of the global average of 92.6%, pointing to challenges in both access to education and learning outcomes. Public spending patterns further underline these concerns. India’s total social sector spending remains around 7.8–8% of GDP, which is modest given the scale of developmental challenges. Education expenditure is estimated at 4.5–4.6% of GDP, below the long-standing benchmark of 6%, while public health expenditure stands at approximately 1.9% of GDP, against the 2.5% target set under the National Health Policy. These gaps in financing translate directly into gaps in outcomes. Investing in education and health is not merely about social welfare; it is an investment in economic growth. A healthier and better-educated workforce is more productive, more adaptable to technological change, and better positioned to support India’s ambition of becoming a high-income economy.

Key Issues in the Health Sector

Despite increased policy attention, several structural challenges continue to affect the health system:

-

High Out-of-Pocket Expenditure (OOPE):

A significant share of healthcare expenses in India is still borne by households, leading to financial distress and, in many cases, avoidance of necessary care. High OOPE undermines equity and pushes vulnerable households into poverty. -

Under-utilisation of Allocated Funds:

In several states and programmes, allocated health funds remain under-utilised due to capacity constraints, delays in procurement, and weak planning at the local level. This reduces the effectiveness of public spending. -

Health Workforce Shortages:

Shortages of doctors, nurses, and allied health professionals especially in rural and underserved areas remain a critical bottleneck. Infrastructure expansion without adequate human resources limits service delivery.

Key Issues in the Education Sector

The education sector faces a different but equally complex set of challenges:

-

Weak Learning Outcomes:

While enrolment levels have improved, learning outcomes remain weak, particularly at the foundational and secondary levels. This raises concerns about the quality of education rather than mere access. -

High Youth Unemployment:

A growing number of educated youth remain unemployed or underemployed, pointing to systemic issues in the education-to-employment pipeline. -

Skill Mismatch:

There is a clear mismatch between the skills imparted by educational institutions and those demanded by the labour market, especially in emerging sectors. -

Inadequate Investment in Teacher Training:

Teacher quality is central to learning outcomes, yet spending on continuous teacher training and capacity building remains insufficient.

What Should the 2026 Budget Focus On?

To address these challenges, the 2026 Budget must adopt a targeted and outcome-oriented approach:

-

Prioritise Primary Health Centres (PHCs):

Strengthening PHCs is critical for preventive care, early diagnosis, and reducing pressure on tertiary facilities. Investments should focus on infrastructure, diagnostics, and service availability. -

Health Workforce Expansion:

The Budget should support training, recruitment, and retention of health workers, particularly in rural and underserved regions, through incentives and improved working conditions. -

Performance-Linked Grants Tied to Utilisation:

Introducing performance-linked funding mechanisms can improve utilisation of health budgets and incentivise better planning and delivery at the state and district levels. -

Align Higher Education with Skilling:

Greater integration between higher education and skill development programmes is essential to address unemployment and skill mismatch. Curricula must be aligned with industry needs and future labour market trends. -

Increased Funding for Teacher Training:

Dedicated funding for continuous professional development of teachers can significantly improve learning outcomes and overall education quality.

Education and health are not competing priorities but complementary investments that determine India’s long-term growth trajectory. The 2026 Budget presents an opportunity to move beyond incremental increases and focus on structural reforms, better utilisation of funds, and outcome-driven spending. A decisive push in these sectors will strengthen human capital, reduce inequality, and support sustainable economic growth.

10. Rajesh Singh, Former Additional Director & Head, Banking & Financial Services, ASSOCHAM

Key suggestions related to the Corporate Bond Market, which are as follows:

India’s goal of becoming a $10 trillion economy by 2030 depends on a strong financial system that can mobilize long-term, low-cost capital to support investment and inclusive growth. A well-developed corporate bond market is crucial for building a balanced and resilient financial system. While India’s corporate bond market has grown significantly over the past decade reaching ₹53.6 trillion in outstanding issuances in FY2025 with nearly 12% annual growth and contributing 15–16% of GDP—it still lags behind peer economies such as South Korea, Malaysia, and China, as highlighted by the NITI Aayog.

To achieve this, there is a need to significantly increase the penetration of the Corporate Bond Market, which requires focused interventions by both the Government and regulators. The key areas that need to be addressed include the following:

- Promote financial literacy to increase a retail participation simplify access of awareness through digital platforms and create retail-friendly bond products. Actual participation in the securities market is very low around 9.5% or 32.1 million households where Urban participation of 15 % and Rural participation stands at 6%.

- Participation of MSMEs is very limited due to high issuance costs and creditworthiness of SMEs’ to access the Debt market. Tax incentives and regulatory reforms will support and motivate to SMEs issuers to enter this market. The Malaysia government has granted stamp duty exemptions for primary and secondary market transactions to encourage bond issuance and trading. Non-residents are exempt from withholding tax on interest income from Malaysian bonds and Singapore grants eligible issuers tax concessions of up to twice the issuance costs for retail bonds, encouraging firms to tap the retail market

- Deepening Municipal Bonds for raising funds for infrastructure.

- There is need to establish a dedicated debt market exchange in India like China’s model (Shanghai Stock Exchange)

- Secondary market bond settlements are currently restricted to RTGS, creating barriers for retail participation. Allowing settlements through alternative payment modes such as UPI, IMPS, and other digital channels would simplify transactions and significantly enhance retail access and participation.

- To encourage greater retail participation, the threshold investment limit for debt instruments should be reduced from Rs. 10, 000/- for all

- To deepen the corporate bond market and improve liquidity, exit mechanisms must be simplified and made more flexible, while encouraging greater participation from treasury houses and institutional investors.

- Regulator Should reduce the Listing fees, introduce credit enhancement mechanisms and widen investor base to improve pricing power.

- Rationalization of LTCG on the sale of Bond Market